YEAR IN REVIEW 2013

Part 2 – US shale gas advantage a game changer for European plastics industry / Players seek to level the playing field but authorities slow to react

The scenario that the US chemical and plastics producers could become self-sufficient in their energy and feedstock supply – music to the ears of companies on one side of the Atlantic – created more dissonant tones on the other side of the pond during 2013. The mood in many ways was reminiscent of the atmosphere of the early 1980s, when executives of major US and European companies cast anxious glances toward the fledgling chemical power Middle East.

With gleaming new production facilities for petrochemicals and plastics taking shape in brand new chemical parks built with the help of Western companies, the Arab world has indeed become an important mecca, but with the rush to force black gold out of American shale deposits and the success that appears within grasp breaking all hype records, the sheiks are increasingly worried about the effects on their business. Even regional powerhouse Sabic is looking for American investment opportunities.

With gleaming new production facilities for petrochemicals and plastics taking shape in brand new chemical parks built with the help of Western companies, the Arab world has indeed become an important mecca, but with the rush to force black gold out of American shale deposits and the success that appears within grasp breaking all hype records, the sheiks are increasingly worried about the effects on their business. Even regional powerhouse Sabic is looking for American investment opportunities.

|

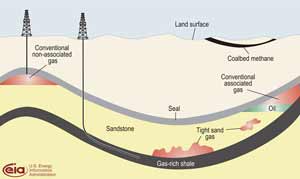

European producers certainly have cause for concern. Already, the gas bill of US competitors is estimated to be less than half of what they pay and far lower than what Asian producers pay. Across North America, pipelines and other transport routes are being put into place and new methods of hydraulic fracturing, or fracking, are extracting greater output – no matter whether the continent’s reserves are as great as purported. US public opposition to fracking, while vocal, is nothing like the outcry on the other side of the Atlantic, and industry and government rarely pay much attention, anyway.

So unpopular is the perspective of being pushed against the wall by competitors brushed off as losers during the prolonged American recession that Europe’s plastics makers, along with gas giants such as BASF subsidiary Wintershall backed by Russian powerhouse Gazprom, are jockeying for position to grab a foothold in potential European shale fields.

So unpopular is the perspective of being pushed against the wall by competitors brushed off as losers during the prolonged American recession that Europe’s plastics makers, along with gas giants such as BASF subsidiary Wintershall backed by Russian powerhouse Gazprom, are jockeying for position to grab a foothold in potential European shale fields.

Germans prudent, French adamant but the UK committed

Lobbying by energy groups on this side of the Atlantic swelled to a crescendo in 2013, though in some places the pleas fell on deaf ears. In a position paper published in April, “The implications of the shale gas revolution for the European chemical industry” the European Chemical Industry Council (Cefic, Brussels / Belgium; www.cefic.org), called for the EU to begin exploiting its own reserves. “The European chemical industry considers that shale gas is an opportunity for Europe. Developing it in a safe and responsible way has the potential to strengthen industry’s competitiveness and create jobs,” Cefic said.

While in Germany, authorities remained as cautious as ever – 2013 was a national election year – and French President Francois Hollande has said that as long as he is president, there will be no exploration for shale gas in France, UK authorities seized the moment and jumped on what they believed to be the gravy train. Poland once again insisted that its train was due to depart any minute after numerous setbacks.

The UK’s commitment to shale gas has grown steadily this year. At the end of 2012, with effect from the New Year, government leaders lifted the moratorium on fracking imposed in 2011 after minor earthquakes racked the Lancashire drilling region. This was despite hefty protests by local councils, environmental groups such as Greenpeace and Friends of the Earth and a myriad of citizen initiatives with colourful names such as “Frack Off” and “BIFF” (Britain & Ireland Frack Free).

Most motivating for the British government was a mid-year report by gas company iGas, (London; www.igasplc.com), licensed to explore gas fields in northern England, stating reserves had been “vastly underestimated.” The slumbering gas had the potential to make the country self-sufficient in gas for 10 to 15 years as well as creating thousands of jobs in economically weak regions, the company said.

While in Germany, authorities remained as cautious as ever – 2013 was a national election year – and French President Francois Hollande has said that as long as he is president, there will be no exploration for shale gas in France, UK authorities seized the moment and jumped on what they believed to be the gravy train. Poland once again insisted that its train was due to depart any minute after numerous setbacks.

The UK’s commitment to shale gas has grown steadily this year. At the end of 2012, with effect from the New Year, government leaders lifted the moratorium on fracking imposed in 2011 after minor earthquakes racked the Lancashire drilling region. This was despite hefty protests by local councils, environmental groups such as Greenpeace and Friends of the Earth and a myriad of citizen initiatives with colourful names such as “Frack Off” and “BIFF” (Britain & Ireland Frack Free).

Most motivating for the British government was a mid-year report by gas company iGas, (London; www.igasplc.com), licensed to explore gas fields in northern England, stating reserves had been “vastly underestimated.” The slumbering gas had the potential to make the country self-sufficient in gas for 10 to 15 years as well as creating thousands of jobs in economically weak regions, the company said.

Reaping long-term rewards for all in Europe but with a promise of environmental safeguards

Poland’s acting environment minister, Piotr Wozniak, told a Warsaw press conference in November commercial exploration in that country could start in 2014. All other recent reports had pegged 2015 as the earliest date large-scale exploration could commence. Even that seemed doubtful to some observers, however, after two North American energy firms ended gas exploration in the country, transferring their franchise to an Ireland-based partner.

It took until nearly the end of the year, but as 2013 drew to a close, the European Commission entered the shale gas discussion, proposing a “have your cake and eat it, too” approach. Janez Potocnik, environment commissioner called for a uniform risk management framework across member states that would allow companies to reap the “long-term economic benefits while assuring critics that fracking carried out with “proper climate and environmental safeguards.” The commissioner said it was unclear whether current EU environmental regulations would apply to shale gas as they were developed before the technology became widely available.

It took until nearly the end of the year, but as 2013 drew to a close, the European Commission entered the shale gas discussion, proposing a “have your cake and eat it, too” approach. Janez Potocnik, environment commissioner called for a uniform risk management framework across member states that would allow companies to reap the “long-term economic benefits while assuring critics that fracking carried out with “proper climate and environmental safeguards.” The commissioner said it was unclear whether current EU environmental regulations would apply to shale gas as they were developed before the technology became widely available.

The future of Grangemouth saved by shale gas? (Photo: George Clerk/iStockPhoto |

In such an uncertain environment, many European plastics players are clearly convinced that the only way to even the playing field with US competitors is to import shale gas – from the US. Ineos, perhaps correctly surmising that the boom could well have passed the company by the time Europe gets its gas reserves out of the ground – if at all – took matters into its own hands in October. CEO Jim Ratcliffe threatened to close the mammoth petrochemical site at Grangemouth if the UK government did not provide financial assistance. The result was nearly GBP 200m in loans and grants from the British and Scottish governments.

But US chemical companies could still get the last laugh. Peter Huntsman, boss of privately owned, Texas-headquartered Huntsman, also understands a thing or two about lobbying. Huntsman came out firmly in favour of “patriotic” efforts to block exports of shale-gas derived ethane and keep America’s precious gas where it belongs – at home.

But US chemical companies could still get the last laugh. Peter Huntsman, boss of privately owned, Texas-headquartered Huntsman, also understands a thing or two about lobbying. Huntsman came out firmly in favour of “patriotic” efforts to block exports of shale-gas derived ethane and keep America’s precious gas where it belongs – at home.

| YEAR IN REVIEW 2013 | |

| Part 1 | General overview (13.12.2013) |

| Part 2 | Shale Gas (17.12.2013) |

| Part 3 | Plastics & Environment (19.12.2013) |

| Part 4 | Plastics Machinery (20.12.2013) |

17.12.2013 Plasteurope.com [227031-0]

Published on 17.12.2013